“Cut your losses, let your gains run…” (just not away)

Having a better methodology for stops and capturing unrealized gains became super important after a certain set of recent disappointing trades. Goldman ran up to an all-time-high of $825.25 ahead of a Jerome Powell speech on September 22, 2025. The positions I held at that point were the result of a few days of analysis, familiarizing myself with more of the statistical properties of the things I am trading—especially in tandem with working through the Quantitative Methods book for the CFA exam in February 2026.

I did a five-year analysis of Goldman’s daily returns dating back to January 2020. They showed 2.36 excess kurtosis and positive skew. In English, that is a stock that has small losses here and there, but a few very large gains. This was a very large gain…and yet I did not capture enough of this move.

I experienced a gain of 584.8% on a GS Oct 2026 800 call after GS rocketed to that all-time-high. Unfortunately, my stop did not hug this position tightly enough and in the subsequent drop gave back nearly half those gains. This was sad and preventable!

What is a “chandelier stop”?

Interactive Brokers’s Trader Workstation offers trailing stops. They are fixed, however. You can set a percentage or a fixed value for the stop. But, then you must through the rigamarole of determining what percentage or absolute value to use. And even after you do that, though, that’s it. The parameter you set for how wide (permissive) or how narrow (restrictive) your trailing stop is doesn’t change.

I have been wanting to understand if having a stop that adjusts dynamically based on an underlying’s volatility made sense. And hey! It turns out this exists and it is called a chandelier stop. I first read about this in Dr. Alexander Elder’s Come Into My Trading Room. It uses the average true range of an underlying to turn volatility into a way to determine where stops should go.

A chandelier stop is set with volatility in mind and may retreat as prices move around. This is basically the mechanical embodiment of breathing room. It can be used for both entries and exits.

As Elder says

When traders are long, it hangs their stops from the highest peak reached by that trend, like a chandelier hangs from the tallest point in the room. As prices move up, the Chadelier Exit, suspended from the highest point of that trend, also rises. It tracks volatility as well as prices, as its distance from the peak grows with the rise in volatility. […] There is no telling how high a trend may go, and a Chandelier will rise until prices peel off from the ceiling and hit that stop.

How much breathing room it has is, of course, the product of the parameters used to create the stop. The chandelier stop consists of a lookback period and the average true range (both to calculate volatility).

Working with Interactive Brokers’s API (v10.37+)

What’s nice is that Interactive Brokers has an API and Python libraries for programmatically interacting with your trading account. The APIs are extensive and take some effort to understand, though. (Some things are not documented very well, others are not documented at all unless you’ve joined a mailing list for support.) Once you get everything running, it is nothing to then start putting on and managing trades via Python—including creating a chandelier stop to manage a long call position that is in the green!

The code below uses Interactive Brokers’s Python library ibapi version 10.37 to execute trades using IBGateway version 10.37 starting in October 2025.

This works, but is also still a work in progress.

ibkr-chandelier.py

# Written to accommodate IBApi libraries 10.30 or above.

# Also built this using 10.37 version of IBGateway.

import os

import time

import datetime

import threading

import pandas as pd

import yfinance as yf

from ibapi.client import *

from ibapi.wrapper import *

from ibapi.contract import *

from ibapi.utils import iswrapper

from ibapi.ticktype import TickTypeEnum

from decimal import Decimal, ROUND_CEILING

ATR_MULTIPLIER = 3 # 3x ATR for stocks, 3-4x for options

ATR_PERIOD = 10 # Standard ATR period

LOOKBACK_PERIOD = 10 # Days to look back for highest high

# Need to round to next nickel to accommodate minimum order tick sizes

def round_to_nickel(price):

return float((Decimal(str(price)) / Decimal('0.05')).quantize(Decimal('1'), rounding = ROUND_CEILING) * Decimal('0.05'))

class ChandelierStopManager:

def __init__(self, ibkr_client, ibkr_account):

self.ibkr_client = ibkr_client

self.ibkr_account = ibkr_account

def _cancel_existing_stops(self, ticker):

# Cancel existing stop orders for a ticker

open_orders = self.ib.openTrades()

cancelled_count = 0

for trade in open_orders:

if (trade.contract.symbol == ticker and trade.order.orderType in ['STP', 'TRAIL']):

self.ibkr_client.cancelOrder(trade.order)

cancelled_count += 1

if cancelled_count > 0:

print(f" Cancelled { cancelled_count } existing stop order(s) ...")

# Calculate a chandelier stop for a given ticker

def calculate_chandelier_stop(self, ticker, multiplier = ATR_MULTIPLIER, period = ATR_PERIOD):

print(f"\nCalculating Chandelier Stop for { ticker }...")

# Download recent price data

data = yf.download(ticker, period = '2mo', interval = '1d', progress = False)

if data.empty:

print(f"Yikes: Could not download data for { ticker } ...")

return None

# Calculate True Range components

high_low = (data['High'][ticker] - data['Low'][ticker])

high_close = abs(data['High'][ticker] - data['Close'][ticker].shift())

low_close = abs(data['Low'][ticker] - data['Close'][ticker].shift())

# True Range = max of the three

true_range = pd.concat([high_low, high_close, low_close], axis = 1).max(axis = 1)

# Average True Range (ATR)

atr = true_range.rolling(period).mean()

current_atr = atr.iloc[-1]

# Current price and highest high

current_price = data['Close'][ticker].iloc[-1]

highest_high = data['High'][ticker].tail(period).max()

# Chandelier Stop = Highest High - (Multiplier * ATR)

stop_level = round_to_nickel(highest_high - (multiplier * current_atr))

# Calculate distance to stop as percentage

distance_pct = ((current_price - stop_level) / current_price) * 100

result = {

'ticker': ticker,

'current_price': current_price,

'atr': current_atr,

'highest_high': highest_high,

'stop_level': stop_level,

'distance_pct': distance_pct,

'timestamp': datetime.datetime.now()

}

# Print results

print(f"\n{ '=' * 50 }")

print(f"Ticker: { ticker }")

print(f"Current Price: ${ current_price:.2f}")

print(f"ATR ({ period }): ${ current_atr:.2f}")

print(f"Highest High ({ period }d): ${ highest_high:.2f}")

print(f"Chandelier Stop: ${ stop_level:.2f}")

print(f"Distance to Stop: { distance_pct:.1f}%")

print(f"{ '=' * 50 }\n")

return result

# Calculate and update Chandelier stops for all open positions

def update_stops_for_all_positions(self, multiplier = ATR_MULTIPLIER):

if not self.ibkr_client.connected:

print("Ooopps! You're not connected to IBKR...")

return

self.ibkr_client.reqPositions()

time.sleep(10)

positions = self.ibkr_client.positions

if not positions:

print("\nNo positions to update")

return

print(f"\n{ '=' * 70 }")

print("UPDATING CHANDELIER STOPS...")

print(f"{ '=' * 70 }\n")

for position in positions:

if position[1] > 0: # Only for long positions

ticker = position[0].symbol

quantity = position[1]

print(f"\n--- Processing { ticker } ---")

# Calculate Chandelier stop level

stop_data = self.calculate_chandelier_stop(ticker, multiplier)

if stop_data is None:

print(f"Skipping { ticker } - could not calculate stop ...")

continue

stop_level = stop_data['stop_level']

# Cancel any existing stop orders for this position

self._cancel_existing_stops(ticker)

# Place new stop order

self._place_stop_order(position[0], quantity, stop_level)

def _cancel_existing_stops(self, ticker):

# Cancel existing stop orders for a ticker

self.ibkr_client.reqAllOpenOrders()

time.sleep(10)

cancelled_count = 0

for trade in self.ibkr_client.open_orders:

if (trade[1].symbol == ticker and trade[2].orderType in ['STP', 'TRAIL']):

self.ibkr_client.cancelOrder(trade[0], OrderCancel())

cancelled_count += 1

if cancelled_count > 0:

print(f" Cancelled { cancelled_count } existing stop order(s) ...")

def _place_stop_order(self, contract, quantity, stop_price):

# Place a stop-loss order

order = Order()

order.action = 'SELL'

order.orderType = 'STP'

order.totalQuantity = quantity

order.auxPrice = stop_price # Stop trigger price

order.account = self.ibkr_account

order.tif = 'GTC'

contract.exchange = 'SMART'

oid = self.ibkr_client.nextId()

# Place the order

trade = self.ibkr_client.placeOrder(oid, contract, order)

print(f" ✓ Placed stop order at ${ stop_price:.2f}")

print(f" Quantity: { quantity }")

return trade

# This is set up to serve as the client and the wrapper

class IBApiClient(EWrapper, EClient):

IBKR_GATEWAY_ADDRESS = '127.0.0.1'

IBKR_TESTING_PORT = 4002

IBKR_LIVE_PORT = 4001

LIVE_DATA = 1

FROZEN_DATA = 2

DELAYED_DATA = 3

FROZEN_DELAYED_DATA = 4

def __init__(self, address, port, client_id):

print("Getting started with IBKR...")

EClient.__init__(self, self)

EWrapper.__init__(self)

# Establish the connection to TWS/IB Gateway

# TWS supports up to 32 simultaneous client connections

self.connect(address, port, client_id)

self.connected = True

self.positions = []

self.open_orders = []

# Launch the client thread

# The 'run' function executes in a loop that repeats as long

# as the client is connected.

thread = threading.Thread(target = self.run)

thread.start()

@iswrapper

def nextValidId(self, orderId):

self.orderId = orderId

@iswrapper

def nextId(self):

self.orderId += 1

return self.orderId

@iswrapper

def currentTime(self, current_time):

t = datetime.datetime.fromtimestamp(current_time)

print(f'Current time: { t }')

@iswrapper

def contractDetails(self, request_id, contractDetails):

attrs = vars(contractDetails)

print("\n".join(f"{ name }: { value }" for name, value in attrs.items()))

@iswrapper

def contractDetailsEnd(self, reqId):

return super().contractDetailsEnd(reqId)

@iswrapper

def historicalData(self, request_id, bar):

print(bar)

return super().historicalData(request_id, bar)

@iswrapper

def historicalDataEnd(self, reqId, start, end):

print(f"Historical data ended for { reqId }. Started at { start }, ending at { end }")

return super().historicalDataEnd(reqId, start, end)

@iswrapper

def error(self, reqId, errorCode, errorString, advancedOrderRejectJson = ""):

print(f'Error: { errorCode }: { errorString }')

return super().error(reqId, errorCode, errorString, advancedOrderRejectJson)

@iswrapper

def tickPrice(self, reqId, tickType, price, attrib):

print(f"Request ID: { reqId }, tickType: { TickTypeEnum.to_str(tickType) }, price: { price }, attrib: { attrib }")

@iswrapper

def tickSize(self, reqId, tickType, size):

print(f"Request ID: { reqId }, tickType: { TickTypeEnum.to_str(tickType)}, size: { size }")

@iswrapper

def tickString(self, request_id, tickType, value):

print(f"Request ID: { request_id }, tickType: { TickTypeEnum.to_str(tickType) }, value: { value }")

@iswrapper

def accountSummary(self, reqId, account, tag, value, currency):

return super().accountSummary(reqId, account, tag, value, currency)

@iswrapper

def updatePortfolio(self, contract: Contract, position: float, marketPrice: float, marketValue: float, averageCost: float, unrealizedPNL: float, realizedPNL: float, accountName: str):

print("UpdatePortfolio.", "Symbol:", contract.symbol, "SecType:", contract.secType, "Exchange:", contract.exchange, "Position:", position, "MarketPrice:", marketPrice, "MarketValue:", marketValue, "AverageCost:", averageCost, "UnrealizedPNL:", unrealizedPNL, "RealizedPNL:", realizedPNL, "AccountName:", accountName)

@iswrapper

def updateAccountTime(self, timeStamp: str):

print("UpdateAccountTime. Time:", timeStamp)

@iswrapper

def updateAccountValue(self, key: str, val: str, currency: str, accountName: str):

print("UpdateAccountValue. Key:", key, "Value:", val, "Currency:", currency, "AccountName:", accountName)

@iswrapper

def position(self, account: str, contract: Contract, position: Decimal, avgCost: float):

self.positions.append([contract, position, avgCost])

print("Position.", "Account:", account, "Contract:", contract, "Position:", position, "Avg cost:", avgCost)

def positionEnd(self):

print("PositionEnd")

def orderStatus(self, orderId: OrderId, status: str, filled: Decimal, remaining: Decimal, avgFillPrice: float, permId: int, parentId: int, lastFillPrice: float, clientId: int, whyHeld: str, mktCapPrice: float):

print("OrderStatus. Id:", orderId, "Status:", status, "Filled:", decimalMaxString(filled), "Remaining:", decimalMaxString(remaining), "AvgFillPrice:", floatMaxString(avgFillPrice), "PermId:", intMaxString(permId), "ParentId:", intMaxString(parentId), "LastFillPrice:", floatMaxString(lastFillPrice), "ClientId:", intMaxString(clientId), "WhyHeld:", whyHeld, "MktCapPrice:", floatMaxString(mktCapPrice))

def openOrderEnd(self):

print("OpenOrderEnd")

@iswrapper

def get_positions(self):

# Get all current positions from an account

if not self.connected:

print("Error: You're not connected to IBKR ...")

return []

positions = self.positions()

print(f"\nFound { len(positions) } open positions")

for pos in positions:

print(f" • {pos.contract.symbol}: { pos.position} contracts @ ${ pos.avgCost:.2f}")

return positions

# Order-related wrappers

@iswrapper

def openOrder(self, orderId, contract, order, orderState):

self.open_orders.append([orderId, contract, order, orderState])

print(f"Order ID: { orderId}, contract: { contract }, order: { order }")

return super().openOrder(orderId, contract, order, orderState)

@iswrapper

def orderStatus(self, orderId, status, filled, remaining, avgFillPrice, permId, parentId, lastFillPrice, clientId, whyHeld, mktCapPrice):

print(f"Order ID: { orderId }, status: { status }, filled: { filled }, remaining: { remaining }, lastFillPrice: { lastFillPrice }, permID: { permId }, avgFillPrice: { avgFillPrice }")

return super().orderStatus(orderId, status, filled, remaining, avgFillPrice, permId, parentId, lastFillPrice, clientId, whyHeld, mktCapPrice)

@iswrapper

def execDetails(self, reqId, contract, execution):

print(f"Execution details. Request ID: { reqId }, contract: { contract }, execution: { execution }")

return super().execDetails(reqId, contract, execution)

def update_once(ibkr_client):

# Example: Connect to IBKR and update stops once

print("\n" + "=" * 70)

print("One-Time Stop Update")

print("=" * 70)

try:

ibkr_account = os.getenv("IBKR_ACCOUNT_ID")

manager = ChandelierStopManager(ibkr_client = ibkr_client, ibkr_account = ibkr_account)

manager.update_stops_for_all_positions(multiplier = ATR_MULTIPLIER)

except KeyError:

print("Yikes! No IBKR account ID available...")

if __name__ == "__main__":

print("\n" + "=" * 70)

print("CHANDELIER STOP SYSTEM ...")

print("=" * 70)

# Connect to Interactive Brokers API via IB Gateway (v10.37 in this case...)

ib_client = IBApiClient(IBApiClient.IBKR_GATEWAY_ADDRESS, IBApiClient.IBKR_TESTING_PORT, 10252025)

time.sleep(7)

update_once(ib_client)

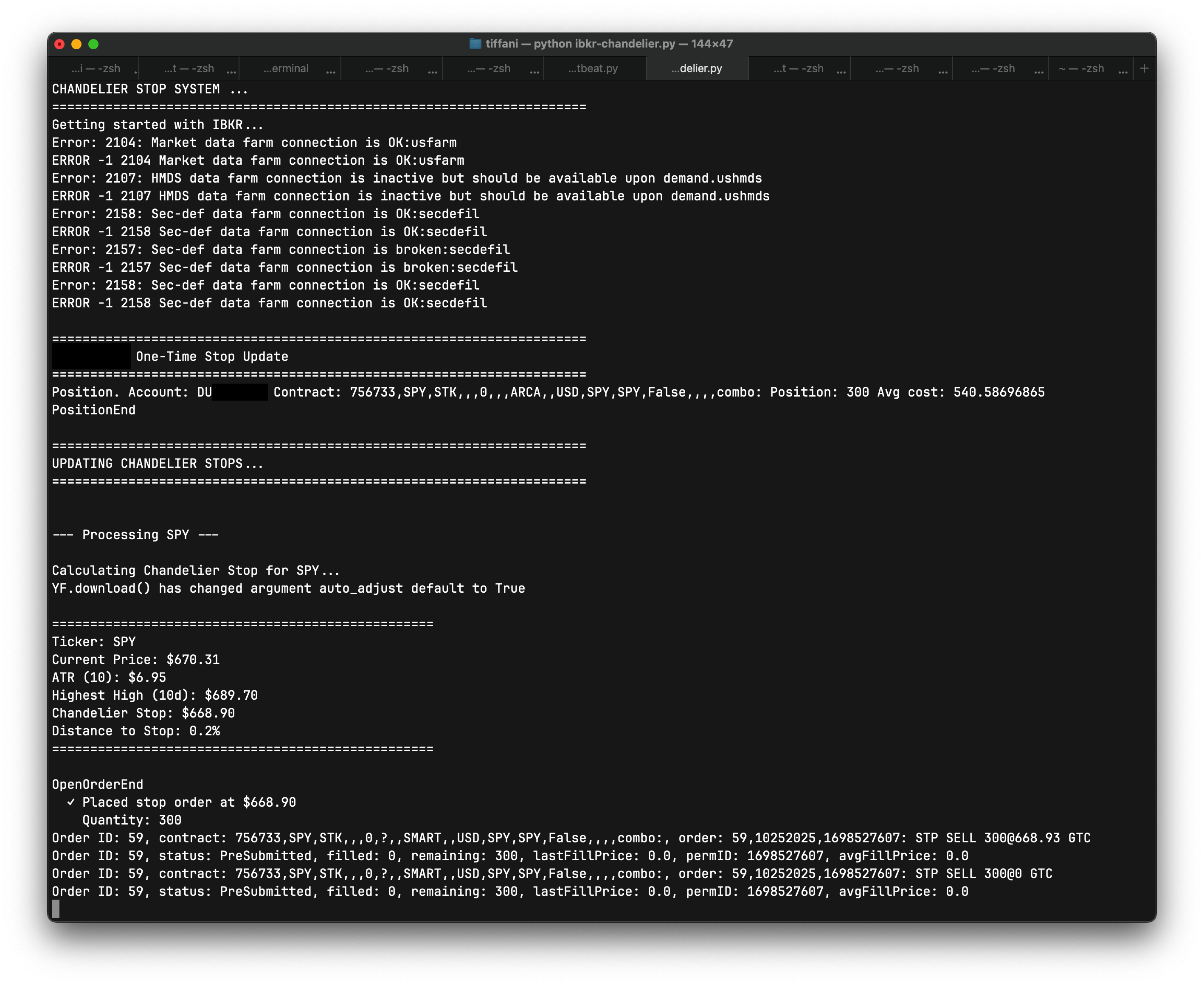

And when it runs, this is what you get! This run is based on my paper trading account with an existing SPY position (shares, not options) I bought when it was at $540.59-ish.

What’s next?

Elder himself admits that the “…negative side of Chandelier Exits is that they give up a great deal of profit. Three Average True Ranges can amount to a lot of money in a volatile market.” He recommends experimenting with the Average True Range coefficient (ATR_MULTIPLIER in my code).

The code listed here does not include the portion that takes a volatility and calculates the option price to set a stop. I will update with that soon.

Finally, some of this code could be cleaned up. The Interactive Brokers API callback methods are mostly from their developer documentation.

An update

Funny enough, this stop triggered right at opening on November 7 after a bad Michigan consumer sentiment reading and tech stock sell-offs. SPY slid to a low of $661.21 after this triggered. There probably could be some work around giving these stops a bit more breathing room (SPY only had to move 0.2% to the downside to trigger it which could easily come from opening volatility some days), but this was still great to see it activate and see SPY continue to fall after this stop was activated, preserving (paper) funds. That really illustrates the power of stops (ignoring stop hunters and quick bouncebacks which could be dealt with by more breating room, etc.).